The Hidden Insurance Gaps That Cause Contractors to Lose Jobs (Even When They’re “Covered”)

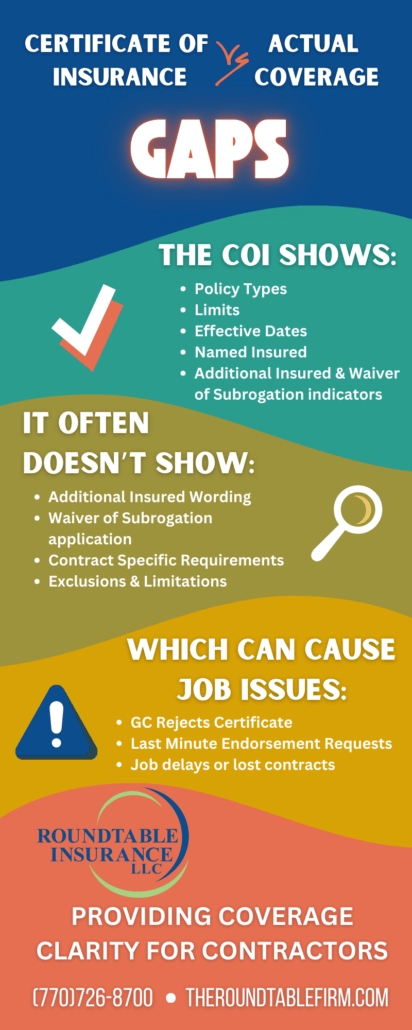

A contractor wins a job, submits their certificate of insurance, and assumes everything is in order. Their certificate shows their General & Excess Liability and Worker’s Comp coverages. They are ready to get to work.

A contractor wins a job, submits their certificate of insurance, and assumes everything is in order. Their certificate shows their General & Excess Liability and Worker’s Comp coverages. They are ready to get to work.

Days later, the general contractor comes back with questions:

- “Can you add us as additional insured?”

- “We need waiver of subrogation.”

- “This coverage doesn’t meet our contract requirements.”

Suddenly, a job that was “secured” is now at risk.

This scenario is far more common than most contractors realize — and it often has nothing to do with price or effort. It happens because certificates don’t tell the full story. Certificates are helpful but when it doesn’t meet the jobs’ requirements the gaps in contractors insurance can lead to a lost opportunity.

Why Certificates of Insurance Create a False Sense of Security

Certificates are often treated as proof of protection. In reality, they’re just a snapshot.

They don’t always show:

- Missing endorsements

- Incorrect additional insured wording

- Coverage limits that don’t align with contract requirements

- Gaps between what the GC expects and what the policy actually provides

This is why contractors can be “covered” — and still lose work.

The Coverage Gaps We See Most Often

Through consultative reviews with artisan contractors, we commonly find gaps in:

- Additional insured endorsements that are too narrow

- Waiver of subrogation not applied across all required policies

- Limits that meet minimums but don’t match exposure

- Policy forms that conflict with contract language

Most brokers don’t walk through these details unless there’s a problem. By then, it’s already impacting your ability to work.

Why This Matters Beyond One Job

Coverage gaps don’t just affect one project — they affect:

- Your reputation with general contractors

- Your ability to bid future jobs

- Your exposure if a claim happens on-site

Insurance shouldn’t just help you qualify for work.

It should help protect the business you’re building.

A Better Way to Approach Contractor Insurance

A proper contractor insurance review focuses on:

- Understanding your contracts

- Aligning endorsements with real job requirements

- Making sure certificates reflect actual protection, not assumptions

It doesn’t have to be complicated — but it does need to be intentional.

Get Coverage Clarity Before Your Next Job

If you’re bidding jobs in Georgia and want confidence that your insurance won’t delay or cost you work, we offer short coverage clarity calls designed specifically for contractors.

These calls focus on:

-

Reviewing contract insurance requirements

-

Identifying common endorsement gaps

-

Making sure your certificates reflect real protection

👉 Schedule a 15–20 minute call to review your current setup before your next project.